INVEST STRATEGICALLY

BY MAYA MARISA JOELSON

BY MAYA MARISA JOELSON

Header

Header

Are you diversified… or are you over-diversified?

If you are invested in a broad range of funds or ETFs, it is likely that you have no strategy.

Something goes up but something else goes down…

You are paying your advisor to tread water – losing out on opportunities to capitalize on structural trends.

Meta Point Advisors cuts through the financial jargon and groupthink to deliver clients’ portfolios that are diversified, transparent, and have a record of beating their financial benchmarks.

Header

If you are the type of investor that has been investing in ETFs, mutual funds, and target date funds, the COVID-19 environment should have made you reconsider your investments and be more strategic – it could have a powerfully positive impact on your portfolio.

As an economist, I’ve always rejected the idea that it is impossible to predict, or at least form an educated opinion, about the profitability of different sectors.

If profitability prediction is impossible, we have been wasting time studying economics and applying business strategy like Michael Porter’s Five Forces.

Header

When I transitioned from being a macroeconomist at a global mining firm to a financial advisor, I warned the attendees at my Harvard Club lecture in 2015 to stay out of energy stocks.

1. Had you followed this advice, your equity portfolio would be 7% higher than if you had stayed invested in energy.

2. It was clear to anyone who understood the oil markets that demand had eroded as China’s infrastructure build receded and oil supply blossomed particularly with the US shale industry.

Header

Now, it should be clear to everyone that entire industries across the economy – airlines, hotels, brick and mortar retailers, and more - face monumental negative demand issues and some are facing bailout, bankruptcy, and permanent closure.

So, why would anyone want to be invested in a broad ETF or mutual fund which includes all these companies facing the precipice?

Even if you had streamlined and just bought sector ETFs of the top two performing sectors of health care and consumer defensives, you still would have lost -9% this year, compared to -14% for the S&P. That’s better, but no cigar.

Header

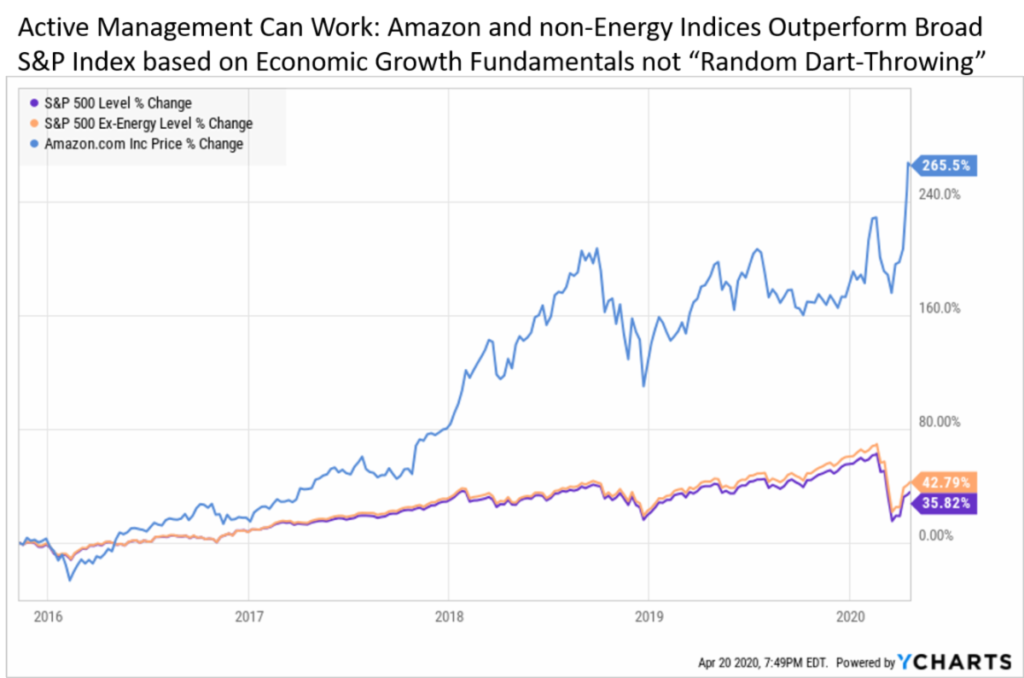

Alternatively, you could have invested strategically in stocks across every industry – and thus had been very diversified – and been significantly up for the year. An easy case in point is had you been invested in Amazon, you would be up 25% for the year but had you invested in its sector ETF of consumer cyclicals, you would be down -34% as off-line retailers shut. This is true across every sector.

It doesn’t take a rocket scientist to anticipate that Amazon and Netflix would outperform given a countrywide lockdown-- though given their lofty valuations, it wasn’t a clear call to buy the stocks. In my opinion, the COVID-era stock winners could single-handedly debunk the notion that stock-picking is just a “Random Walk Down Wall Street.”

Header

Of course it is nearly impossible to pick all the top stocks, but there were 72 stocks in the S&P 500 (or 15% of total) that were either flat or positive for 2020. There were 201 stocks (34%) that performed better than the S&P index. It was even easier to eliminate the losers for 2020, further increasing the probability to pick a portfolio of stocks that would beat the market indices. Moreover, if it is in a taxable account, you can offset the winners with the losers to reduce your capital gains taxes as I explained in my article “Are you Missing Out on Tax-Loss Harvesting and other Single Stock Benefits?”

Header

Morningstar and many financial advisors like to separate stocks into value and growth. As an economist, I don’t espouse this approach because it obscures the underlying dynamics driving the industries in these broad-based indices. For instance, both energy and financials tend to be in value indices. Yet, energy stock prices are driven by oil prices but financial stocks’ profitability is more dependent on interest rates. For stocks dropped into value territory, for example, you need to separately analyze whether or when demand for those companies' products and services will return and whether the companies have the cash or prospects for financing to weather through a downturn.

Header

Analyzing the sectors themselves would provide better information on the future profitability of the stocks in these sectors. Without teasing out the core drivers, it is easy to fall into a “value trap” in which you buy stocks because seem cheap but in fact are priced that way for a good reason. You may be able to more than double your money if the company succeeds, but if not, you could lose all of your investment.

Financial pundits often like to say there will be a rotation from growth stocks, which have dominated the last decade, toward value stocks. They use mean reversion as a rationale that are ostensibly grounded in statistics. I think the concept of mean reversion is often overused as an intellectual crutch in the context of the stock market.

Header

So if broad-based ETFs aren’t working, what about mutual funds whose raison d’etre is to actively pick stocks? Well, the vast majority of mutual fund managers have underperformed ETFs for the past decade, which is why ETFs became so popular. But the reason mutual funds might underperform is not because active management can’t work but because mutual fund structures and cultures impede savvy active managers.

Here are a few issues to consider:

1. High fees – Mutual funds can add an extra ~1% annually to your fees.

Header

2. Benchmark hugging – Question: What’s the #1 goal of a mutual fund manager? Answer: Not to lose his job. So, how does this play out in the marketplace? The mutual fund manager chooses stock allocations that are very close to the index benchmark. MSCI was the top performing stock in the financials space in 2020 -- perhaps the result of fund managers who still have to pay MSCI for index data. The end result of benchmark hugging is that too often mutual funds often closely mirror their indices so they have a similar performance to an ETF but they are weighed down by higher costs (see point #1).

3. Not nimble – Drastically switching stocks in the portfolio had to be done in a few days to have the best effect. Mutual fund companies are simply too slow to make these drastic changes in a timely manner.

Header

4. Bureaucratic, slow decision-making – Analysts do in-depth work on companies, creating financial models. Analysts need to convince fund managers to implement their new buy and sell recommendations. These discussions often occur on a set timetable that may be too slow to implement in a timely manner in a fast moving market.

5. Inefficient trades that move the market - Even if portfolio managers agree to implement changes in their stock positions, the sheer size of the trades will move the market price in the wrong direction for the fund (buying stocks at increasingly expensive prices while selling at increasingly lower prices). This also drags down performance.

Header

6. Higher capital gains you pay are often unwarranted – Let’s say you invest in a mutual fund because it has outperformed its peers. However, the fund manager may have invested 5% in Tesla, which has more than doubled since the prior year. Fund guidelines may say he can’t have more than 10% of the portfolio value in a single stock. So he has to sell Tesla. What happens? He sells Tesla and you, the new mutual fund owner, have to pay taxes on the Tesla capital gains sale even though you never benefitted from the appreciation of the stock. Investing in stocks avoids this problem as investors only have to pay taxes on gains they actually benefitted from. As redemptions to mutual funds increase with the flow to ETFs and out of the market, remaining mutual fund holders are primed to suffer from even more passed-on capital gains that they can’t control. In contrast, when I buy a portfolio of strategic stocks for you, all your capital gains and losses will be directly related to your own portfolio and based on your needs.

Header

7. Limited tax-loss harvesting - Mutual funds tend to pass along more capital gains than losses. As well, they send along capital gains and losses based on their needs, not yours. In contrast, I can work you based on your expected annual income, risk tolerance, and ESG preferences to generate tax gains and losses that best fit your needs.

8. Mandate limitations - Many mutual and hedge funds must conform to a predetermined mandate even if the world changes and they think that they could preserve or make money better with another strategy. It is better to work with a financial advisor who can adapt your portfolio based on your requirements, preferences, and goals.

Header

We are in a regime shift that we have never seen before. As the situation changes, it makes sense to have a wealth advisor who can shift your portfolio to best position you for the new reality.

Please contact me if you want to discuss more and how this applies to you.

Header

When the markets give you lemons, it’s time to make lemonade.

The last quarter of 2018 was the first time in decades that all major asset classes declined at the same time -– the US stock market went down ~10%, almost every international market went down more than 10% except Brazil and India, and even US bond funds were no longer a safety play as the benchmark AGG went down — 3%, as I warned would happen at the beginning of the year in this newsletter and in my interview with The Wall Street Journal. But for some investors, there is a silver lining to stock market losses – the ability to sell those losses to lower your tax bill to Uncle Sam.

I suspect some of the extreme market volatility at the end of 2018 can be attributed to hedge funds and others conducting tax-loss harvesting. Have you gotten into the action or have you missed out on this opportunity? Unfortunately, many investors have been lured into buying supposedly diversified index and mutual funds that often have too many accumulated gains and so little dispersion that you cannot benefit from tax-loss harvesting.

Header

Suppose you have the good fortune of earning or inheriting a large concentration of a single stock. For example, perhaps you received Apple stock 10 years ago, which has since risen 1,110%. Suppose your holdings were worth $1 million at the beginning of the year. If you wanted to sell it in order to diversify your stock holdings or make a purchase of a home, you would have to pay an estimated $200,000 in capital gains taxes – assuming that your cost basis was very close to zero and you are in the top tax bracket.

Now, imagine you “diversified” this holdings into an index that tracks the S&P index fund. Alternatively, you can “diversify” the holdings into a basket of individual stocks such as the top 25 stocks in the S&P. What would be the difference in your financial situation by the end of 2018 given these separate approaches to diversifying your US stock holdings?

1. Your portfolio would have performed 7% better by investing in the top 25 S&P stocks over an S&P Index. If you put $40,000 into each of the top 25 S&P stocks at the beginning of 2018 (for a total investment of $1 million), your portfolio would have lost 5% vs. -12% had you put your investment in S&P indices like SPY and VOO. You would be almost $70,000 and 7% better off by investing the top market cap stocks.

Header

2. More winners: If you invested in the top 25 stocks, 10 of your stocks would have gained on the year 2018 – most notably Merck up 26%, Amazon and Mastercard up 15% each, and Pfizer and Microsoft up over 10%. Again, no major asset class or international market (except India up 5% and Brazil up 11%) gained on the year.

3. Greater dispersion and diversification: While Merck was up 26% in 2018, Facebook was the laggard down 30% on the year. This 56% dispersion between holdings is almost impossible to spot if you only have conglomerated ETFs and mutual funds. Yet, the greater dispersion implies better diversification and less correlation, providing more opportunities to match gains to losses in order to lower your tax bill and rebalance your portfolio with new opportunities. This is what I was able to do for my clients as the market tumbled.

4. If you did not tax-loss harvest, you would have to pay $200,000 for year-end 2018 taxes because you sold your Apple stock at the beginning of the year. This is another 20% loss.

Header

5. However, if you did tax-loss harvest, you could save over 2.4%. Index funds boast small fees but they don’t have the advantages of holding individual stocks. As well, you can carry over your losses to future years.

6. In years when the S&P 500 is flat to up, there are few tax-loss harvesting opportunities. Therefore, most years you are better off in a basket of stocks if you want to tax-loss harvest. Some robo-advisors have claims about their tax-loss harvesting strategies with ETFs but their tactics are questionable and the SEC fined Wealthfront and others for false claims regarding their tax-loss harvesting strategies.

7. In years in which the S&P 500 is down, you can tax-loss harvest, but at the risk of losing out if there's a big upswing in the markets.* If you buy the same security in a 30-day period after selling it, you forfeit the ability to recognize a loss on your tax returns, according to what's known as the wash-sale rule – so had you sold earlier this month, you would not be able to buy to take advantage of today’s 1,000-point upswing.

Header

8. Owning a basket of individual securities means you can rebalance your portfolio and tax-loss harvest every year to reduce your taxation. For instance, at the beginning of the year, many portfolios had a high overweight in technology given tech stock outperformance in the past few years –- wise investors took some of the gains in high-flying tech stocks offset by poorer performing stocks to lock in their gains and rebalance their portfolios. This is what I did for my clients.

9. Owners of mutual funds generally fare even worse in tax-efficiency. Most mutual funds make year-end capital gains tax distributions that shareholders in the fund must pay. Even in years when the market is down, these capital gains can be high. American Funds declared a 9-11% expected capital gains distribution on its Growth Fund of America. If you had put your $1,000,000 into mutual funds like this, you could have another ~10% or $100,000 in capital gains on which you would have to pay taxes. As these holdings would have been for less than a year, it is considered a short-term gain and you would have to pay a much higher ordinary income rate on this $100,000 gain.

Header

These are just a few of the reasons that owning a basket of stocks can achieve a better pre-tax and after-tax performance than owning a “more diversified” index or mutual fund. Skilled active stock picking and management can improve the performance -– for instance, if Facebook were sold on July 25, 2018, the stock would have been up 23% on the year and thus have dodged its end of December fall of almost 30%.

Please let me know if you would like to learn more about my approach to single stock, single bond, and income alternative investing and how you can benefit from greater transparency, tax-efficiency, performance, and risk management.

* This analysis is based on data from Ycharts on YTD price performance of VOO, SPY, and the top 25 stocks in the S&P 500 as of December 26, 2018. The market subsequently shot up 1000 points but is dropping the following day so this analysis is as of the data accessed end of day December 26, 2018.

Header

ESG funds — the acronym stands for environmental, social, and (corporate) governance — have been around for a while. They attract investors who want to do good in addition to doing well financially. And since George Floyd’s death in the spring of 2020 bringing with it an increased interest in social justice, ESG funds have seen their assets under management climb to over $1 trillion in 2020.

But does this money actually flow to socially responsible investments? If you care whether your money is being invested in companies that reflect your values, it pays to look beyond the flashy ESG label.

All too often, it turns out, investors who want to create societal change through ESG funds are often just supporting more of the same.

sults?

DO ESG INVESTMENTS PRODUCE SUPERIOR RESULTS?

While the ESG index excludes tobacco and weapons producers and claims it is “sector-diversified and targets high ESG ratings in each sector,” the composition of the index closely resembles that of a broad exchange-traded fund, or ETF.

ESG funds often do slightly outperform the index, but this can largely be attributed to their exclusion of the faltering oil industry and not the ability to capitalize on the strengths of diversity.

A public company named MSCI, spun out of Morgan Stanley, has become the de facto entity that sets the industry benchmark for ESG index and active funds. MSCI designed its index to “maximize exposure to positive environmental, social and governance (ESG) factors while exhibiting risk and return characteristics similar to those of the MSCI USA Index.”

That sounds great on paper, but the reality is not as righteous.

But ESG funds support diversity, right?

You might expect that, but the top companies on the MSCI ESG list have long been in the spotlight for a noticeable lack of racial and gender diversity in the workplace.

Take Microsoft, which tops the MSCI ESG index, and which Forbes criticized for its “grim” diversity statistics: much like the tech sector at large, Microsoft’s workplace is over 75% male and 60% white; Apple and Amazon offer similarly homogeneous environments. Microsoft’s CEO recommended that "women shouldn't ask for raises, and instead, rely on karma to propel their careers forward." Karma! As of fall 2019, Microsoft’s women were still in legal battles for pay equity. The company's black employees leaked memos to the media to pressure their CEO to support Black Lives Matter.

Take Microsoft, which tops the MSCI ESG index, and which Forbes criticized for its “grim” diversity statistics: much like the tech sector at large, Microsoft’s workplace is over 75% male and 60% white; Apple and Amazon offer similarly homogeneous environments. Microsoft’s CEO recommended that "women shouldn't ask for raises, and instead, rely on karma to propel their careers forward." Karma! As of fall 2019, Microsoft’s women were still in legal battles for pay equity. The company's black employees leaked memos to the media to pressure their CEO to support Black Lives Matter.

Actively managed ESG funds did not show a substantial difference in investments than passively invested funds that track the ESG index. Forbes calculated that the $2.3 billion held in actively managed ESG mutual funds had its largest holdings in Microsoft, Alphabet, Amazon, and Apple.

Why are ESG funds so focused on these companies when there are other, more socially conscious tech companies? Marc Benioff, CEO of Salesforce, led the push for a San Francisco tax on big companies, to be used to combat homelessness and publicly pay women on an equal footing with men. Yet Salesforce does not show up in the top investments for socially responsible investment indices.

Why haven’t ESG fund managers paid attention to the lack of diversity of the companies they invest in?

That’s an excellent question — especially since a company’s governance and social consciousness are supposed to be among the criteria for ESG investments. But it’s hard to see a problem when you’re looking in a mirror.

While diversity in the tech industry is bad, it’s even worse in wealth management.

In 2004, I wrote the first paper for the World Economic Forum on the business case for women and diversity “Why the Advancement of Women is Strategically (and not just Politically) Correct”. Since then, the World Economic Forum launched its highly regarded Global Gender Gap Report and McKinsey, Gartner and other prestigious firms have shown statistically that diverse teams result in better financial outcomes. The industry has had more than a decade to incorporate this information and diversify itself, but little has changed for white women and people of color. Dive into the current statistics and it’s clear that too often claims of diversity are the corporate equivalent of lipstick on a pig.

People of color and white women manage just 1% of assets in the United States, a percentage that hasn’t budged since the early 1970s. More than half of college graduates are female, but only 14% of financial advisors are women; the majority are still confined to administrative roles. That’s what happened to me when I graduated from Wesleyan in the 1990s. In the World Financial Center, I was trapped in Working Girl while the men were playing Wolf of Wall Street. It wasn’t until I came back to finance with graduate degrees from Northwestern and Harvard that Wall Street hired me into a non-secretarial role.

The appalling diversity statistics in wealth management should alarm anyone with a 401(k) or a financial advisor. There are over 270,000 financial advisors managing trillions of dollars in wealth – including yours, either directly or through retirement funds, equity share plans, or any number of financial instruments. These financial advisors are overwhelmingly male and pale, with an investment approach driven by the groupthink of their boy’s club workplaces. Their white male echo chamber leads to myopic investment strategies and investors pay the price.

Men make up 90% of portfolio managers and 91% of active fund managers have underperformed their respective benchmarks for 15 years. MarketWatch reports that men have gotten 85-90% of the new roles in mutual funds even though data shows that women equally perform or outperform men and have more credentials like the CFA.

It makes sense that if women and minorities represent over 50% of the marketplace, that all-white male investment teams cannot run successful investment portfolios given their gigantic blind spots. So how do wealth managers respond? They lower client expectations. They advise clients that it is impossible to beat the market and shift the conversation to “goals-based” planning and their next golf outing.

Given these statistics, investors who actually care about diversity should look more closely at their wealth management teams. Take Morgan Stanley, a firm that paints itself as a leader in ESG. On June 18, former Morgan Stanley Chief of Diversity Marilyn Booker sued the company for racial discrimination and harrassment. Booker claims Morgan Stanley offered only superficial support for her diversity efforts, and never took seriously the importance of fostering an inclusive workplace.

It takes work to research companies that reflect your values and can provide you a substantial return. Find an advisor who shares your commitment and walks the walk, not just talks the talk. Check out the diversity of your financial advisory team and move your money to a more equitable team or a diverse advisor who is likely superior given s/he has been able to survive in a hostile industry without the handouts that their white male peers often receive.

Even companies that claim to care about supplier diversity do not apply that lens to the teams managing their lucrative corporate equity compensation, 401(k) plans, and pension funds. Too often, an investment bank takes a company through its IPO and these lucrative corporate plans fall into the lap of the overwhelmingly all-white male wealth management team that the same firms have anointed to provide these services. Even supposedly socially conscience pension funds have invested to the ~$100 billion with Ken Fisher who has likened attracting clients as akin to trying to get into a woman’s pants and later issued a statement that he often uses such “colorful” language.

Currently, the good old boys are regaled with awards based on years of service and assets under management, not investment performance. The title of “Top Advisor” is like a modern-day version of the landed gentry. A retiring advisor (almost always a white man) has accumulated accounts over his 40+ year career and anoints someone to take over his accounts and, with it, the title of “Top Financial Advisor.” If it’s not actually his son, it’s usually someone who looks like him. People of color and women usually get left out of this game.

Even publicly traded firms that tout their diversity continue to give wealth management teams leeway to hire whomever they wish, so they hire people who will “fit” on the team. Why add a woman to your advisory team if you can no longer “let loose” at team drinks? Especially if you already have one woman on your team? Why add a young black man if he doesn’t have rich parents to bring on as clients? Firms claim they are acting as fiduciaries to clients but they are not ensuring that the best person gets the job and that clients are best served. All those guys who thrived in Wolf of Wall Street cultures, they are now rewarded for their “years of experience” while women and minorities are essentially shut out. CNBC just launched its "Top Financial Advisors" list and its top pick went to Salem Investment Counselors, which controls over a $1 trillion and surprise! (not) all of its 10 investment advisors are white men, mostly aged.

The UK government recently successfully launched mandatory gender pay gap reporting for all firms with over 250 employees. This mandatory, uniform reporting exposes financial firms’ true data to be held accountable for hires, fires, and promotions across all roles. With mandatory, standardized reporting, firms will find it harder to cherry-pick their numbers to project a diverse image when the reality is overwhelmingly male and pale. Mandatory reporting should extend to race as well as gender across all roles.

“How diverse is the financial advisory team working on my investments?”

“How well did they perform in growing and protecting my savings?”

Keep asking questions until you’re satisfied —because this diligence can pay off for you. It is possible to be a socially responsible investor and outperform the market. I know. My clients have been rewarded for trusting their savings with me despite my nontraditional packaging.

Elite and expensive male-dominated hedge funds continue to trail their benchmarks. My clients’ portfolio performance is over 25% better than that of Bridgewater, the world’s largest hedge fund — which is being sued for gender discrimination by its former CIO.

Despite Bridgewater’s poor performance and disputed ethics, the firm’s founder Ray Dalio told The Wall Street Journal that there is, “a waiting list to invest” in his flagship fund.

It is encouraging to see that clients are seeking socially responsible investments but clients need to move their money where their mouth is and stop investing with the status quo who have benefited from an unequal playing field. Those who do may likely be rewarded with advisors who can outperform the status quo, because they have had to fight harder and smarter to survive in this business. I can’t tell you how many investors I have met who won’t leave their financial advisor because he’s “a nice guy,” “my golfing buddy,” or “like a brother to me,” while I see their financial statements and see how much money this “nice guy advisor” has underperformed the market and charged them underhanded commissions.

Unless society and clients demand change from their investment advisors and the wealth management industry, minorities and women will never have an equal opportunity to become a “Top Advisor,” no matter how skilled they are. Trillions of dollars are currently being passed down in the financial industry from (usually white male) advisor to (probably white male) advisor.

Are you going to start rewarding talent or keep rewarding the status quo? Both your conscience and your wallet will thank you if you demand equal opportunity in the finance industry.

Please contact me if you want to talk more about your investment goals. I’m also thinking of establishing a real ESG task force. Let me know if you’d like to consider working on this.

Maya Marisa Joelson founded Meta Point Advisors after several years at Merrill Lynch. She is a Harvard-trained economist who leverages her two decades of top-level experience across advanced technology, Wall Street, and emerging markets to devise investment strategies for her clients.

Maya’s clients benefit from her ability to provide savvy active management without the cumbersome costs and structure of mutual funds. Maya enjoys working with her clients to understand their personal needs so she can craft tailored financial plans. Maya’s investment views have been featured in The Wall Street Journal and Barron’s.

Maya excels at deriving “meta points” from economic and market data. She strives to apply these insights to achieve superior outcomes for her clients. Her ability to abstract important concepts and communicate them has differentiated her, whether writing about Russia’s conversion to capitalism while at Harvard, women in business at the World Economic Forum, equity markets in London’s hedge fund community, or collaborative technologies for DARPA program managers.

Maya holds an MPA from Harvard Kennedy School, MBA from Kellogg at Northwestern University, and a BA from Wesleyan University.

We'd love to hear your thoughts on what you have read here. Please don't hesitate to reach out to us with feedback or questions.